All Categories

Featured

Table of Contents

For many people, the biggest problem with the boundless financial concept is that initial hit to early liquidity brought on by the expenses. This con of unlimited banking can be minimized significantly with correct policy layout, the initial years will always be the worst years with any type of Whole Life plan.

That stated, there are certain boundless financial life insurance policies designed largely for high early money worth (HECV) of over 90% in the very first year. The long-term performance will frequently substantially lag the best-performing Infinite Financial life insurance policy policies. Having access to that extra 4 figures in the initial few years might come with the price of 6-figures in the future.

You in fact obtain some considerable lasting advantages that assist you recover these early costs and after that some. We find that this prevented early liquidity trouble with boundless financial is much more mental than anything else as soon as thoroughly checked out. As a matter of fact, if they absolutely required every dime of the cash missing from their boundless financial life insurance coverage policy in the first couple of years.

Tag: limitless banking concept In this episode, I speak about finances with Mary Jo Irmen who shows the Infinite Financial Idea. This topic may be debatable, but I intend to obtain varied sights on the program and learn more about different techniques for ranch monetary management. Some of you might agree and others will not, but Mary Jo brings a truly... With the rise of TikTok as an information-sharing platform, economic guidance and methods have discovered a novel way of dispersing. One such strategy that has been making the rounds is the boundless banking idea, or IBC for short, garnering endorsements from stars like rapper Waka Flocka Fire. While the technique is currently popular, its roots map back to the 1980s when economic expert Nelson Nash presented it to the globe.

Within these plans, the money worth expands based on a rate set by the insurance provider. When a considerable money worth collects, insurance policy holders can obtain a cash worth finance. These financings differ from standard ones, with life insurance policy acting as security, suggesting one can lose their protection if loaning excessively without adequate money value to sustain the insurance expenses.

And while the attraction of these plans appears, there are inherent constraints and risks, necessitating thorough cash value tracking. The technique's legitimacy isn't black and white. For high-net-worth individuals or local business owner, particularly those utilizing methods like company-owned life insurance policy (COLI), the benefits of tax obligation breaks and substance development could be appealing.

Bank On Yourself Review Feedback

The attraction of boundless financial doesn't negate its obstacles: Cost: The fundamental requirement, a long-term life insurance policy plan, is more expensive than its term equivalents. Eligibility: Not every person qualifies for whole life insurance policy due to extensive underwriting procedures that can exclude those with particular wellness or way of life problems. Complexity and danger: The elaborate nature of IBC, coupled with its dangers, might deter several, particularly when easier and less risky options are offered.

Alloting around 10% of your monthly earnings to the plan is just not feasible for lots of people. Making use of life insurance policy as an investment and liquidity resource requires discipline and surveillance of policy cash worth. Consult a financial advisor to identify if infinite banking lines up with your concerns. Component of what you read below is simply a reiteration of what has currently been said over.

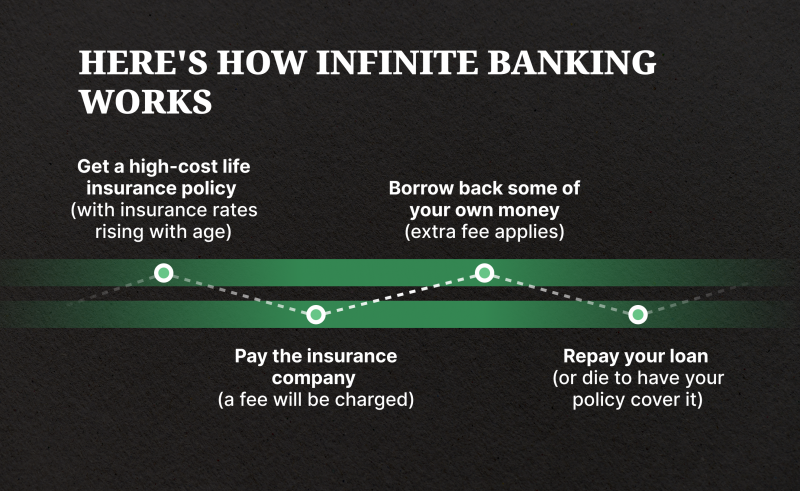

Prior to you get on your own right into a circumstance you're not prepared for, understand the complying with first: Although the concept is frequently offered as such, you're not in fact taking a car loan from on your own. If that were the case, you would not have to settle it. Rather, you're obtaining from the insurer and need to repay it with passion.

Some social media sites posts advise making use of money worth from entire life insurance policy to pay for charge card financial debt. The concept is that when you repay the lending with interest, the quantity will be sent out back to your financial investments. Sadly, that's not exactly how it works. When you pay back the loan, a part of that passion goes to the insurer.

For the initial numerous years, you'll be repaying the compensation. This makes it extremely hard for your policy to gather worth during this time around. Entire life insurance policy prices 5 to 15 times much more than term insurance coverage. The majority of people just can not afford it. Unless you can afford to pay a couple of to a number of hundred dollars for the next decade or more, IBC won't function for you.

Become Your Own Bank Book

Not every person must depend exclusively on themselves for economic safety and security. If you need life insurance policy, here are some beneficial pointers to take into consideration: Think about term life insurance policy. These policies offer coverage during years with substantial financial obligations, like mortgages, pupil finances, or when taking care of children. Make certain to look around for the ideal price.

Copyright (c) 2023, Intercom, Inc. () with Reserved Font Style Name "Montserrat". Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Booked Typeface Call "Montserrat".

Build Your Own Bank

As a CPA focusing on actual estate investing, I've cleaned shoulders with the "Infinite Financial Principle" (IBC) extra times than I can count. I have actually even spoken with professionals on the topic. The main draw, besides the apparent life insurance policy benefits, was constantly the concept of accumulating money value within a long-term life insurance policy plan and loaning versus it.

Certain, that makes sense. But truthfully, I always assumed that cash would be better invested straight on financial investments rather than channeling it through a life insurance policy plan Till I found how IBC could be integrated with an Irrevocable Life Insurance Trust (ILIT) to produce generational wealth. Allow's begin with the essentials.

Infinite Bank

When you obtain against your policy's cash worth, there's no collection repayment schedule, giving you the flexibility to manage the lending on your terms. On the other hand, the cash worth remains to expand based upon the policy's assurances and dividends. This configuration enables you to accessibility liquidity without disrupting the lasting growth of your plan, provided that the car loan and interest are managed carefully.

As grandchildren are birthed and grow up, the ILIT can acquire life insurance coverage policies on their lives. Family participants can take fundings from the ILIT, using the money value of the plans to fund financial investments, start companies, or cover major expenses.

An important facet of managing this Family Financial institution is using the HEMS standard, which stands for "Wellness, Education, Maintenance, or Support." This guideline is commonly consisted of in trust fund arrangements to direct the trustee on just how they can distribute funds to recipients. By adhering to the HEMS criterion, the count on ensures that distributions are produced vital needs and lasting support, protecting the count on's possessions while still attending to relative.

Increased Versatility: Unlike inflexible bank loans, you control the settlement terms when obtaining from your very own plan. This permits you to framework payments in a way that lines up with your company money flow. infinitebanking.org. Improved Cash Flow: By funding overhead with policy finances, you can potentially maximize money that would certainly otherwise be tied up in traditional loan settlements or devices leases

He has the very same tools, however has likewise developed extra cash value in his plan and got tax benefits. And also, he currently has $50,000 offered in his plan to make use of for future possibilities or expenses. In spite of its possible benefits, some individuals remain cynical of the Infinite Banking Idea. Allow's attend to a couple of usual worries: "Isn't this simply costly life insurance?" While it holds true that the costs for an effectively structured whole life policy might be greater than term insurance coverage, it is necessary to watch it as greater than just life insurance.

Infinite Banking Example

It's regarding creating a flexible financing system that offers you control and provides multiple benefits. When made use of purposefully, it can complement other financial investments and business strategies. If you're intrigued by the potential of the Infinite Financial Principle for your organization, here are some steps to take into consideration: Educate Yourself: Dive deeper right into the principle with trusted publications, workshops, or consultations with knowledgeable experts.

{kind=link}

Latest Posts

Banking Life Insurance

How To Take Control Of Your Finances And Be Your Own ...

Unlocking Wealth: Can You Use Life Insurance As A Bank?